How to grow revenue—a business owner’s cheat sheet

.png)

There is no more important job in your business than finding the people who will pay you money. Without someone constantly working on that, there is eventually no business.

In the early days, that might mean pursuing any kind of customer. But as your business matures, you'll get smarter, and realize that a dollar is not a dollar is not a dollar. That is, there is good money and bad money, just as there are good expenses and bad expenses. And that random revenue is less valuable than predictable revenue. Your long-term success hinges on knowing why people buy, where those people can be found, and what you can do in the short term to cover costs if revenue falls.

In this guide, we’ll share a business owner’s cheat sheet to generate more good revenue based on our work advising 3,000+ businesses and monitoring billions of dollars in transactions each year.

Within you’ll learn to:

- Recognize bad money

- Reevaluate your customer

- Simplify your pricing and packaging

- Streamline your sales process

- Revisit your offers and marketing

- Increasing your revenue

- Turning revenue into margin

What is good money vs bad money?

Let’s say someone invests $2 million in your business and now you just have that money in the bank. Is that good money or bad money? It really depends.

If you have a good business model and the expertise to reliably turn $1 into $5, that debt could be good money, because you have a good chance of growing your business and paying it all back. But if you took that money without a plan, will soon have to start paying it back, and are scrambling to cover payroll, that’s bad money. It’s only going to make the pressure worse.

It also somewhat depends on who your investor is. If that investor is kind and introduces you to important people, the money may be good money. But if they’re dictatorial, short-sighted, and interfere with the company, it may be bad money.

Customers can also offer good money or bad money. If a customer demands so much from your workers that it makes them want to quit, that customer’s money is bad money. Whereas customers who make the place better—who pick up after themselves, leave good reviews, and make a habit of visiting your store, their money is good money.

It may go without saying but you want to build a business that reliably makes good money. Good money makes the company easier and easier to run.

Now, saying no to bad money may sound like a luxury if you’re just starting out and happy to have any customers at all. But multi-time business owners will attest: It’s smart to think about this from the start. If you start out attracting bad-money customers, and they make the environment intolerable, it becomes difficult to change. Good employees won’t want to work there, or won’t last.

So with that understanding, how do you grow good revenue? In four ways.

Four ways to grow revenue and sales

We recommend following these four steps in order—starting with your customer and ending with your marketing. That’s because if you don’t have the right customers, no amount of Google Ads can save your business. And if you don’t have the right offerings for those right-fit customers, no amount of loyalty coupons will keep them coming back. If you take the time to get the slow, boring pieces right, everything else gets a lot easier. People will finally respond to your ads because they know, like, and trust you.

The following advice varies a lot depending on the business type—you’ll want to tailor this to your situation. If you’re curious about getting help building your business plan, earning more sales, and growing, talk to a Pilot CFO.

1. Reevaluate your customer

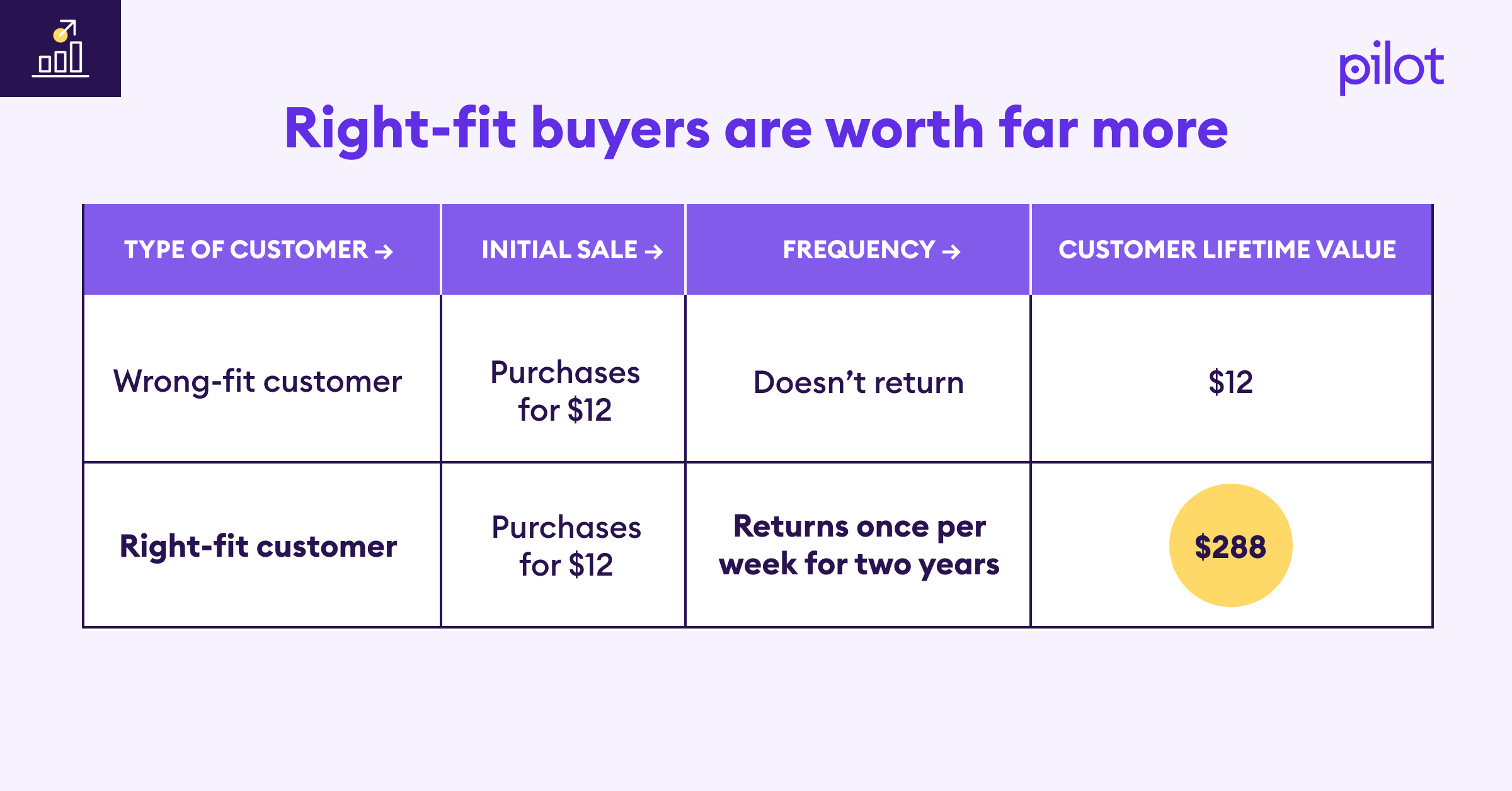

Do you really know who your ideal customer is? Not just the people who walk in, but the ones who spend “good money”? If you run a cafe and it’s filled with people working on laptops all day, those might seem like your ideal customers. But how much do they each really spend? If they nurse one cappuccino for six hours while the local crew of firefighters are in and out, always buy pastries, and spend 2x more, you should be interested in the firefighter types.

This becomes clear if you look at customer lifetime value instead of customer acquisition cost. In the example below, both customers cost the same to acquire—let’s say $4.

You want to build everything about your business to serve those ideal people. Provided, of course, there’s a large enough population to sustain you. Those ideal customers can help you generate more revenue and refer friends at a higher rate, and you see this all the time with coffee shops, which use decor to signal “who they are for.”

Consider Saint Frank, a boutique coffee shop in San Francisco. They are unapologetic about not offering WiFi on weekends. They don’t allow dogs except service animals. (Though they have a cute sign about it.) This is because they want to keep a sanitary interior for their ideal customers who love quiet, orderly spaces. Most people buy a coffee. But Saint Frank’s ideal customers don’t flinch at spending $24 on an espresso tasting flight. And those people want to find a seat, so Saint Frank can’t have all tables occupied by people working.

When you act like Saint Frank and signal to one group that you are “for” them, you are also telling other customers that you are not for them. At Saint Frank, many people probably hesitate at the menu and the prices. That may make you, as the owner, nervous. But counterintuitively, the more you tailor the business to those ideal customers, the stronger those ideal customers feel about you—and the more they spend and the more they refer.

Very often, those ideal customers can more than offset the loss of other customer types.

This works across industries. Todd Nienkerk has run the web design agency Four Kitchens for 19 years, and when we asked him what he learned in that time, this was among his top takeaways: Be for someone. Which means being not for others. “Do that and you’ll never be short of business,” he says.

How do you know who your ideal customers are? You probably already have some intuition, but it can really help to interview people. Ask customers, or run a survey with a QR code, and if people complete it, they get a modest 10% discount.

Ask customers:

- How’d they find you?

- Why’d they buy?

- How’d they make that decision?

- Do they sometimes buy elsewhere?

- What’d cause them to buy 100% of the time from you?

- What’d cause them to stop being a customer?

- What could you do to attract more people like them?

You can also use some point-of-sale systems or advertising platforms like Facebook or Google Ads to look at your customers’ demographics: age, gender, location, spending habits, and more.

Use that information to build a “profile” of your ideal customer. You may have several types.

When you serve the right customers and signal to them that your establishment is “for” them—whether an agency, cafe, or food startup—order sizes go up. And your marketing starts to resonate more.

2. Simplify your pricing and packaging

Over time, all businesses tend to overcomplicate their prices and packaging. Eventually, their menu of offerings starts to look like this:

If you give people too many choices, they get decision paralysis. They decide not to decide. They linger at the entrance and then move on. Whereas new businesses tend to earn a lot of press for having very few offerings. When McDonald’s launched, it was interesting to consumers because it only offered nine things.

Today, the McDonald's menu has 145 items. But you should never confuse what a giant corporation does now with what it did to become massive. Don’t copy their menus or their ads, which by the way, are what big companies do to defend market share. You have better, more direct forms of marketing including “word of mouth.” Plus, you can’t do it all. It’s smarter to do fewer things well and become known for that.

For example, many service businesses like moving companies, yard maintenance, and pest control can get their start simply by doing one thing better than the competition. An all-inclusive moving company where there are no options or decisions is actually easier to buy from—and more memorable.

Simplifying your pricing and packaging also saves you money

Here’s the beauty of simplifying your pricing, packaging, and offerings: Not only does it make it easier for people to buy, but it also costs you less to deliver. Rather than stocking many items, you only need to keep a few. Rather than training many specialized employees, you just need a handful—and less training. When you simplify your “menu,” you also simplify your cost structure.

Not only does it make it easier for people to buy, but it also costs you less to deliver.

What’s the difference between pricing, packaging, and offers?

You have several levers you can pull to simplify what you sell. You can adjust the price, the packaging, or the offer:

- Price is the dollar value.

- Packaging is the quantity.

- Offer is the framing.

Here’s an example: A creative agency’s pricing might be $250 per hour, but their base package is 20 hours. That’s their pricing and packaging. The owner can then wrap that in an offer—which makes it more attractive to their clients—because nobody really wants to buy their time per se. They want the outputs: the website and brochures. So the creative agency can create an offer called “new business starter kit.”

While you’re at it, can you launch higher margin offerings?

While you are considering simplifying, why not sell more of the services or products that make you the most money? Use a spreadsheet to analyze your profit margin on your various services and offerings and compare them. The results may surprise you. Delis, for example, make a significant portion of their profit from “impulse purchases” like gum and candy. It seems cheap, but the margin is high. What’s your version of an impulse item? Can your consultancy have an “audit” add-on that seems cheap to the customer, but is virtually free for you to deliver?

What’s your version of an impulse purchase that doesn’t cost a lot, but is very high margin, that people can add on during checkout?

The steps to reevaluate your pricing:

Compare your pricing to the market

Research the pricing strategies of your top competitors. Analyze how their pricing has evolved in response to current market conditions. Talk to your prospective and existing customers to get a sense if they’ve evaluated your competitors’ pricing. Seek to understand why your customers choose your product/service relative to other options, and how they make those decisions.

Quantify customers’ perceptions of your product/service

Can you put a dollar value to how much customers like you versus the competition? Evaluate how customers perceive the value of your product or service. Use customer surveys, focus groups, and sales data to understand their price sensitivity and willingness to pay.

Adjust pricing

Based on your findings, develop a strategy to make small adjustments and/or offer new tiers. Get feedback and ensure your strategy considers both the competitive landscape and the way customers perceive your value.

Test and iterate

Implement small-scale pricing tests to gauge customer response before a full rollout. Monitor sales and customer feedback closely to assess the impact of these changes.

Communicate the change

Do not simply raise prices, unless the amount is small. Communicate why the change is happening, and frame it in terms of why it’s actually good for your ideal buyer: To offer them better service, to improve the quality, or at the very least, ensure you can stay in business.

Monitor people’s reactions

Stay alert and see how customers and competitors react, if at all.

3. Streamline your sales process

Is your business difficult to buy from? Secret shop yours and find out. Very often, owners are shocked at how disconnected their employees are from what drives customer loyalty and revenue, and how difficult they make it to buy. Whereas very small changes to that checkout or consultation can make a significant impact in your revenue.

The payment platform Stripe has studied this rigorously and finds that simply offering people additional payment options at checkout, online or in-store, can increase conversions 7.4%. Imagine an additional 7.4% in sales just by checking a box.

If someone wants to give you money, you should:

- Respond fast.

- Explain the process.

- Set expectations.

- Do what you say.

Doesn’t matter how big or small you are—consultancy or cafe. It’s your job as owner to make buying as easy as it can be.

Purchasing from you should be as easy as possible—which was one of Amazon’s early secrets: one-click checkout. The only reason to introduce friction into the buying process is if it serves a purpose, which yours may.

If you run a professional services business and your employees will be going into someone’s home, you want to be sure that person is prepared. Have them fill out a questionnaire and sign a waiver. Or perhaps you run a marketing agency that can only help consumer goods companies—you’ll want to force buyers to talk to a salesperson before signing a contract so you can be sure you can actually deliver.

It’s also worth noting that streamlining the sales process doesn’t just benefit the customer but also the owner. Standardizing the process reduces the cost to serve customers, speeds up the cash conversion cycles through faster invoicing or tighter payment terms, and can help your revenue just as much as, say, the site design.

All to say, make buying easy and more people will.

4. Revisit your offers and marketing

Once you know your buyer, have the right pricing and packaging, and have simplified your sales process, now it’s time to discuss marketing. But there are many misconceptions about what marketing is, so let’s start there.

Marketing exists to make people aware of what you offer and its benefits. It requires what psychologists call “theory of mind,” or understanding what’s going on in your customer’s head. To you, they may be purchasing plushie dollars from your ecommerce site. But to that buyer, they’re celebrating their daughter’s birthday. The more you can get inside your buyer’s head, the smarter you can market.

Good marketing is all about the “offer,” which we discussed briefly in the pricing and packaging section. If you run a flower shop and February 14 is around the corner, offering a Valentine’s Day special is smart marketing. And it’s even smarter marketing if you have ready-made bouquets with a sign that says, “Don’t forget Valentine’s Day—we won’t tell.” Now you’re solving a present need for your buyer, framed in a way that the value is clear.

How to increase revenue with marketing

Find what already works and do more of it

Rather than invent something new, look to what already works. Are you starting to get referrals from ChatGPT? Write more answer articles on your website. Do people tend to refer you to friends? Offer a two-way referral discount. If marketing is about running experiments, repeat ones that have already worked.

Test that your offers are clear

Take a screenshot of your current ads and offers and show them to someone who matches your ideal buyer. This could be a friend or a peer. Tell them you didn’t make those ads (to get an honest response). Ask what they think—what’s their unfiltered reaction?

Hold yourself back from explaining—you won’t be there to explain the offer in the wild. Keep testing and iterating until you have good offers that truly do speak for themselves—and are immediately clear.

Be specific

Use evocative words, numbers, and quotes—they tend to convert better. “Save $300 per year” is a better offer than “Affordable service.”

Stand out

You cannot win at marketing by copying competitors—even if you’re selling a commodity. In fact, the stranger and more distinct you are, the more memorable, and the fewer marketing messages someone needs to see to remember you. For example, the sports team the Savannah Bananas are intentionally ridiculous and you only need to see them once to know they exist.

True differentiation, which could mean investing in a brand identity, can help you charge more. Take the beverage company Liquid Death. They sell water. Same water as everyone else. But they charge $1 more, and people are thrilled to pay it because the “brand” solves a problem other waters don’t: People don’t like being at concerts or festivals drinking from a clear plastic water bottle when everyone else is drinking alcoholic beverages. It makes them feel apart. So they’re more than willing to pay a little extra to have a can that looks more extreme.

Include a call to action

You can get everything else about your marketing right, and it still doesn’t work simply because people don’t know what to do with that information. You see this all the time with billboards advertising a top lawyer, but there’s no contact information. Or the website font is too small to read.

Whenever you are marketing, always tell people precisely what to do next:

- Give us a follow

- Book now

- Download your copy

- Visit our store

- Talk to our sales team

- Book your free consultation

Marketing channels to consider

- Social media—Facebook, Twitter, SnapChat, TikTok, YouTube

- Search marketing—Google Search, Bing, ChatGPT, Claude

- Content marketing—blogging, podcasting

- Email marketing

- Running a newsletter

- Flyers and door hangers

- Digital ads

- Print ads

- Billboard and out-of-home (OOH) ads

- Radio ads

- Newsletter ads

- Signature ads

Increasing revenue means knowing what levers to pull—and teaching others

With everything you now know, you can see that increasing revenue is about a lot more than just running ads. You need to target the right people, come up with compelling offers, and write calls to action that are clear enough that people can actually act on them. Your job is to use all that to build a revenue “machine” that consistently drives more sales. And hopefully, with less and less of your effort.

Many owners learn to generate revenue instinctively, but it’ll be crucial for you to document what you know works, so you can pass that knowledge on. This is the crucial breakpoint: Can you create a sales team that doesn’t need your constant support? Many businesses get stuck at $1 million per year because the owner is so necessary, and they can’t be everywhere at once. A business where the founder does all the selling can only grow so large.

That’s why the final step here is to document what works so you can train others and build repeatable systems. What have you learned about your ideal customers? What packages seem to work in what seasons? Where do buyers get stuck in your sales process? What marketing has worked in the past, and which hasn’t?

Start modestly—just by keeping notes—and eventually you’ll want to build out training, program, and even incorporate AI to handle some pieces of this process, like generating offers and graphics. When you reach the point where that system works without you, you know you’ve built something that can grow.

Revenue growth only matters if it increases cash flow and margin

We want to see all of this effort pay off for you—so don’t lose sight of the “good money.” And what that means is, you should be keeping some of the money. Many business owners chase topline revenue growth at all cost and take on too much “bad money” and though they double their sales from $1 million to $2 million in a year, they spend so much on materials and contractors that in the end, their earnings are the same. Or even less.

This is part of why running a business is so difficult, but also one you’re ready for. You, as the owner, are the best-positioned to find all the balances that help you grow your revenue sustainably.

Want help strategizing more ways to generate revenue? Talk to a Pilot CFO. We’ve helped thousands of companies like yours understand their customers, create sales systems, and increase their revenue.

Miss!

%20(1).png)

.png)