2025 Year-End VC Market Insights

In H2 2025, the venture market made real progress, but the recovery wasn’t felt equally across the board. Deal activity picked up and valuations rose, but capital remained selective and fundraising outcomes were still shaped by liquidity constraints.

We were cautiously optimistic in 2025, and that outlook carries into 2026. The broader signals are encouraging – liquidity is improving and exit markets are gaining momentum – but fundraising will likely stay competitive and take longer than founders are used to, with the strongest outcomes going to the top performers.

In this environment, we’re focused on helping founders extend runway, sharpen their capital strategy and use-of-funds narrative, and build the financial foundation they need to raise successfully in an improving market.

If you have any questions or ideas for our next issue, please let me know at Neha.Banik@CFO.Pilot.com.

We’re here to help and would love to hear your thoughts.

5 Trends You Need to Know

- Runway outcomes in 2025 were divergent across cash-burning tech companies. Pilot proprietary data showed a growing share of companies faced near-term liquidity pressure, with 26% holding less than six months of runway (up from 20% in 2023).

- AI drove the market, representing ~65% of VC deal value and ~40% of deal count, underscoring that it was not just a megadeal story but also powered a large share of overall activity. Investors have become increasingly comfortable backing exceptional AI talent with outsized first checks.

- Early-stage activity rebounded in H2 2025, with first financings and early-stage rounds nearing 2021 highs, signaling renewed investor appetite for new company formation. This reflects a shift from caution to selective conviction, as investors re-engage earlier in the company lifecycle.

- In 2025, VC recovery was uneven: liquidity remained limited, and capital access remained selective outside the top tier. As a result, financial discipline and capital efficiency became key differentiators for companies navigating fundraising and future liquidity.

- Valuations stabilized in 2025, with median pre-money valuations rising across stages, driven by the return of higher valuation multiples and a more favorable macro backdrop. Yet, pricing power remained concentrated among top-tier companies.

Pilot Proprietary Data Trends

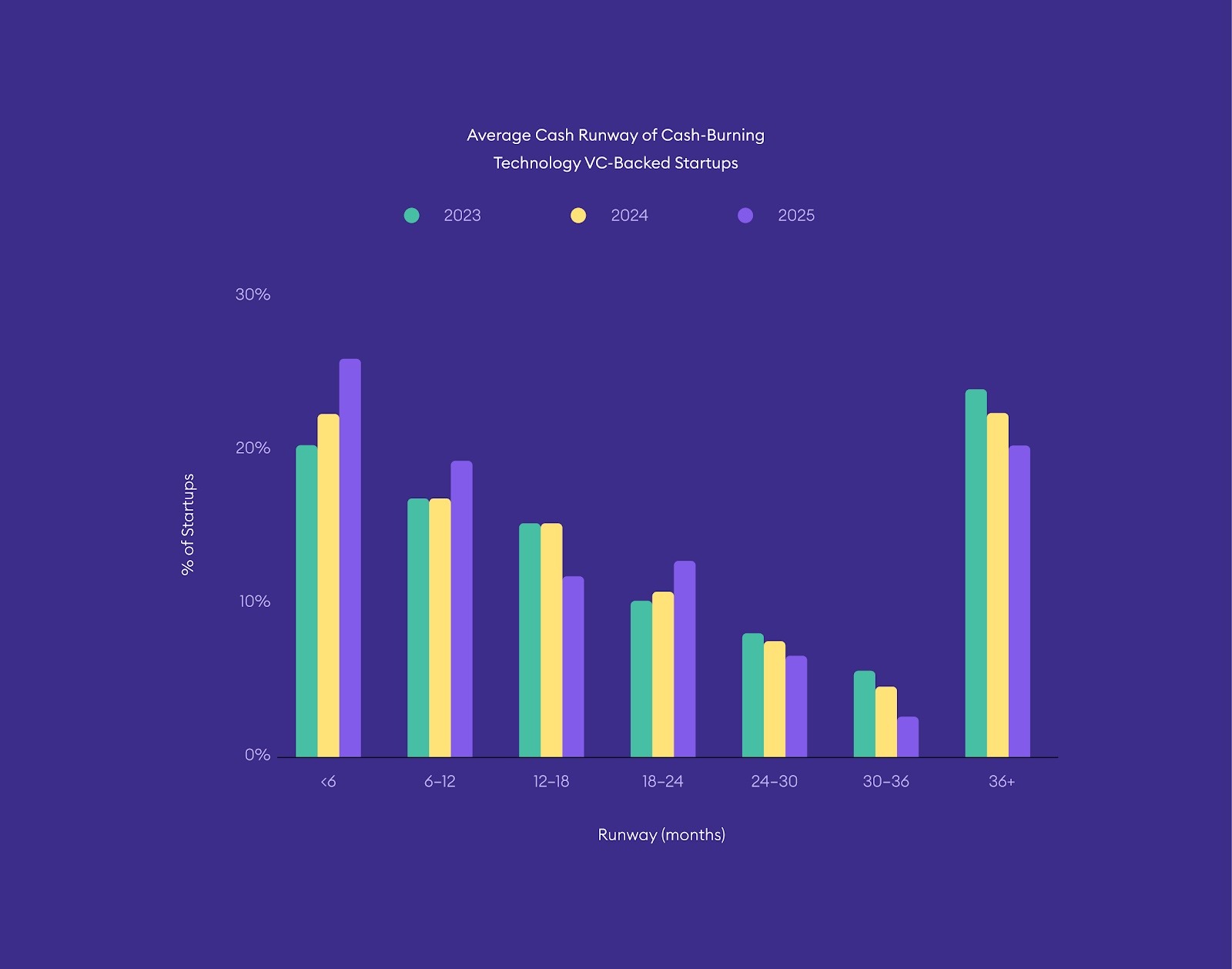

Cash Runway

Pilot proprietary data showed rising % of companies with <6 months of runway, signaling growing liquidity pressure

The share of companies with less than six months of runway increased to 26% (up from 20% in 2023), and 57% had under 18 months of runway, pointing to mounting near-term liquidity pressure.

At the same time, the share of companies with more than 36 months of runway remained limited, suggesting that extended liquidity is increasingly concentrated among companies that either secured meaningful funding or reduced burn early.

Although runway is a lagging indicator, these trends highlight early signs of stress in the broader venture ecosystem, reinforcing the need to monitor fundraising outcomes alongside operational performance.

VC Market and Fundraising Trends

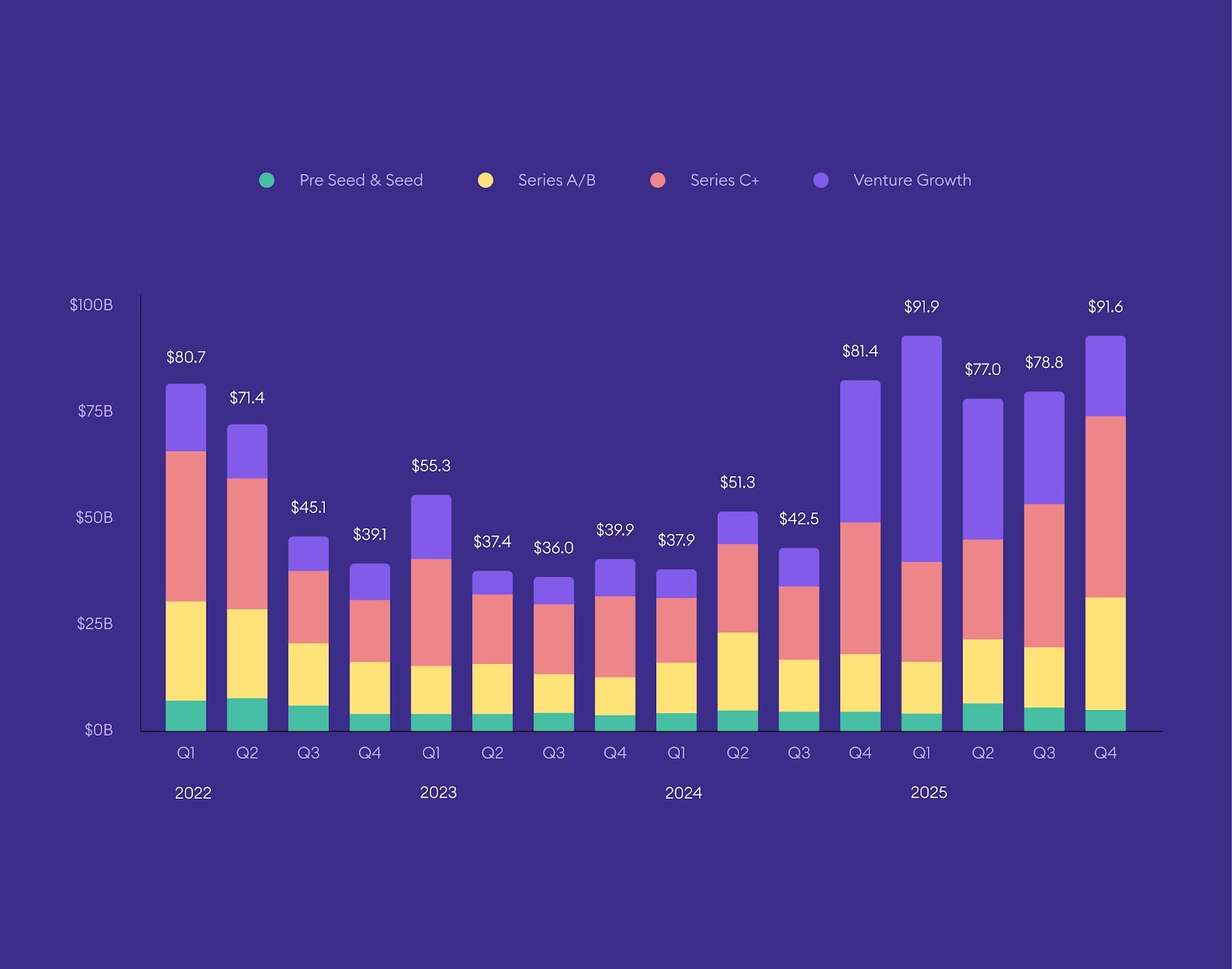

VC Deals by Value

Deal value rebounded in 2025, driven by AI mega deals & concentrated momentum

In FY 2025, total US VC deal value reached ~$340Bn, making it the second-highest year of the past decade, trailing only 2021. The rebound was heavily concentrated in later-stage activity: late-stage VC and venture growth deal value rose 45.4% and 131.1% YoY, respectively, supported by a small number of outsized transactions, particularly in AI.

Q4 capped the year with $91.6Bn deployed across an estimated 4,482 deals. AI continued to anchor total dollars in Q4: 11 rounds reached or exceeded $1Bn, and the top 11 deals totaled $37.4Bn (41% of quarterly value).

Notable Q4 raises, including Anthropic’s $15Bn round and Project Prometheus’ ~$6Bn first financing, illustrate how a small number of AI-led transactions are driving a disproportionate share of total deal value.

VC Deals by Count

Deal count rose in 2025 across stages, even as investors remained selective

In FY 2025, US VC deal count increased to ~16.7K deals, up from ~15.2K in 2024. Deal counts increased at each stage, with first financings and early-stage rounds nearly reaching 2021 and 2022 highs, indicating renewed investor appetite for new company formation.

While more companies got funded, the increase in deal count reflects measured re-engagement, not relaxed underwriting. Investor activity remains highly selective, with capital deployment skewed toward sectors with clear long-term conviction, limiting access for companies outside these profiles.

VC Deals by Industry

AI continued to dominate: 65% of FY 2025 deal value and 40% of deal count

In FY 2025, AI was the defining driver of venture allocation, representing 65.4% of total VC deal value and 39.4% of total deal count. This is not just a megadeal story: AI & ML was the #1 vertical by deal count for the second year in a row.

Beyond AI, the activity mix remains concentrated in software and digitally native categories. By deal count, the leading verticals in 2025 included SaaS, Healthtech, Fintech, and Mobile. By deal value, AI & ML leads again, followed by SaaS and Big Data, with Manufacturing and Life Sciences also ranking highly by dollars deployed.

Capital allocation has become increasingly theme-driven. As a result, sector alignment now plays a materially larger role in fundraising outcomes than stage or company maturity alone.

VC Supply vs Demand Imbalance

Market conditions improved, but access to capital remains limited for late-stage

While venture market conditions became more founder-friendly over the course of 2025, the improvement has not translated into balanced access to capital. Half of all VC dollars in 2025 were concentrated in just 0.05% of completed deals, underscoring an extreme mismatch between capital supply and startup demand.

Later-stage companies (Series C+) are facing the sharpest effects of this imbalance. With investor capital concentrated in a narrow set of high-conviction themes, many scaled startups are extending runways, prioritizing profitability, and reassessing growth trajectories to avoid down-round financing in a constrained fundraising environment.

If you have any questions or suggestions for the next issue, please reach out to the Pilot Consulting Team: Neha.Banik@CFO.Pilot.com

Miss!